Answering your questions

FAQS

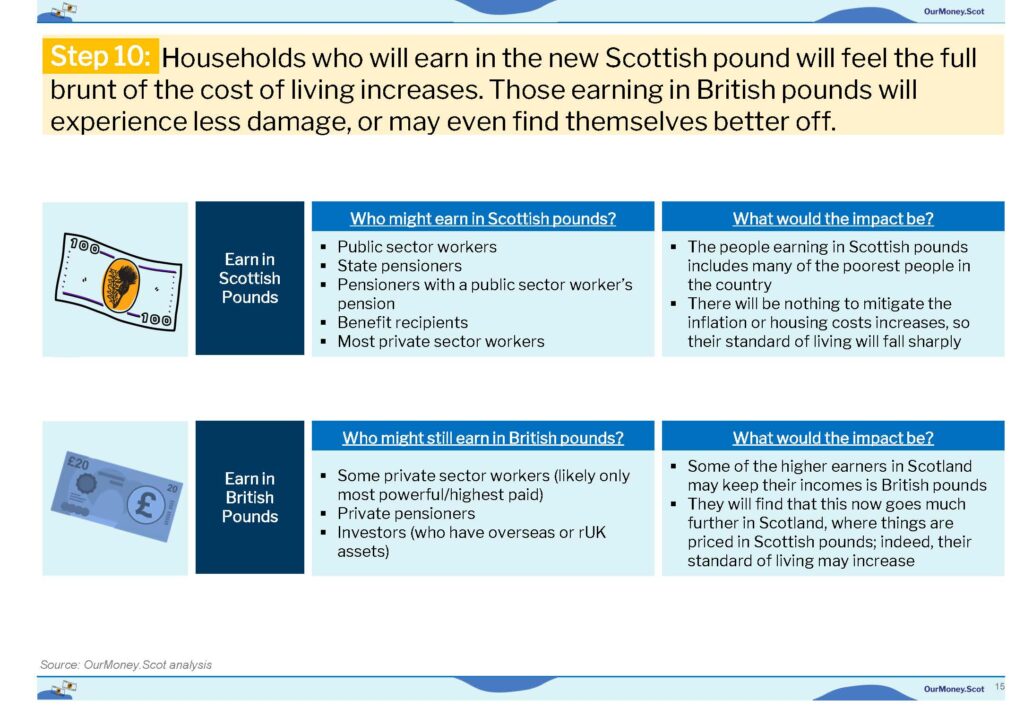

How we calculated your results

Our Methodology

Professor Ronnie Responds

Our Analysis

Many thanks to those who have tried out the tool, and engaged with our analysis.

We would like to keep updating this site and using it as a place to explore some of the issues around currency and Scottish independence. New data will emerge, further details of plans will be announced and colleagues will contribute to and challenge our analysis.

One of the goals of Our Money is to keep the conversation around currency at the heart of the debate about Scottish independence. In that spirit, we wanted to answer some of the questions that we’ve seen come up over the past couple of weeks, and provide some more details about our analysis.

The SNP says that after a transitional period where Scotland keeps using British pounds, it will introduce its own currency. The timeline for this is not provided by the Scottish government – they say it will happen ‘as soon as possible’ and will be determined when a set of (currently undefined) criteria are met around fiscal sustainability, institutional preparedness and market credibility.

However, the Scottish government does not have the luxury of setting its macroeconomic policy in a vacuum. Lending markets will have a keen eye on Scotland as it treads a path towards independence. It is our view, based on the extensive international finance literature, that these markets will force the shift to a new devalued Scottish currency far more quickly than the Scottish Government suggests. The problem is this: the First Minister is proposing that lenders hand over billions pounds worth of sterling to an independent Scotland. However, because she is also proposing Scotland moves to a new currency, she cannot guarantee to those lenders that they will be repaid in Sterling, or at all.

The markets have a habit of decrying this kind of uncertainty. They would likely create pressure (for example by increasing debt costs for Scotland) that would act to force Scotland’s hand and push it towards a more sustainable settlement – its own currency. This would most likely be immediately following independence if not before.

As the widespread evidence on historical devaluations demonstrates, once this new currency is introduced, it is our view that a depreciation would persist until the underlying fundamentals point in a different direction. In the immediate days following a devaluation exchange rate changes would likely be volatile, as foreign exchange markets often are in response to big events, and overshoot ‘fair value’. Ultimately, the ‘fair value’ of Scotland’s currency would be 20-30% lower than the British pound, and the valuation would trend towards this level.

I would expect the devaluation to persist until the underlying macro fundamentals changed and, particularly, the balance of payments deficit. If the standard traditional trade elasticity conditions hold, the currency depreciation in itself should help to address the balance of payments deficit although will take time and will need to be supported by conservative fiscal policies if the Scottish Government wished to turn the devaluation round over time. There is also the possibility, due to the so called ‘J curve’ effect that Scotland’s Balance of payments deficit would worsen in the short term.

The Scottish government may well indeed seek to peg the value of the Scottish pound to the British pound (or Euro) when the currency is launched, but it would need to ensure that the value set for the currency was at a fair value. This would require them to set the currency in the 20-30% devaluation range that we have referred to. Otherwise they would face a very costly speculative attack on the currency which would result in the classic combination of high interest rates, currency depreciation and massive foreign exchange rate losses. Crucially, also it would need to have its own central Bank with the institutional structure to run such a regime including the ability to print money.

By pegging a country’s currency to other currencies, the Scottish Government would be giving an unlimited commitment to defending the currency at the pegged rate. This means that the rate at which you peg has to be at fair value and that you need to have very large foreign exchange reserves to defend the peg to counter any potential speculative attack and have macroeconomic policies which are in line with a pegged rate. Other countries that peg their currency have foreign exchange reserves in the range of 20% (Denmark) to 60%+ (Singapore) of GDP and run conservative fiscal policies in order to generate the necessary foreign exchange reserves, which are a form of national saving. Indeed, most countries that peg their exchange rate run fiscal surpluses which would certainly curtail the flexibility of macroeconomic policy-making.

Few countries build their foreign exchange reserves by borrowing, as suggested by The Scottish Government in its recent economic statement for an independent Scotland. It is not a credible policy to financial markets and is often a signal that a currency is about to be subject to a speculative attack.

What Would this mean for me?

As one of Scotland’s – and the world’s – leading economists and currency experts, Ronnie has set out the currency options for a newly independent Scotland. Now take the test to find out what they would mean for you.